Trial Lawyers, Inc. v. Public Markets

Todd Zywicki argues the US' "litigation environment amounts to a de facto tax on participating in public markets"

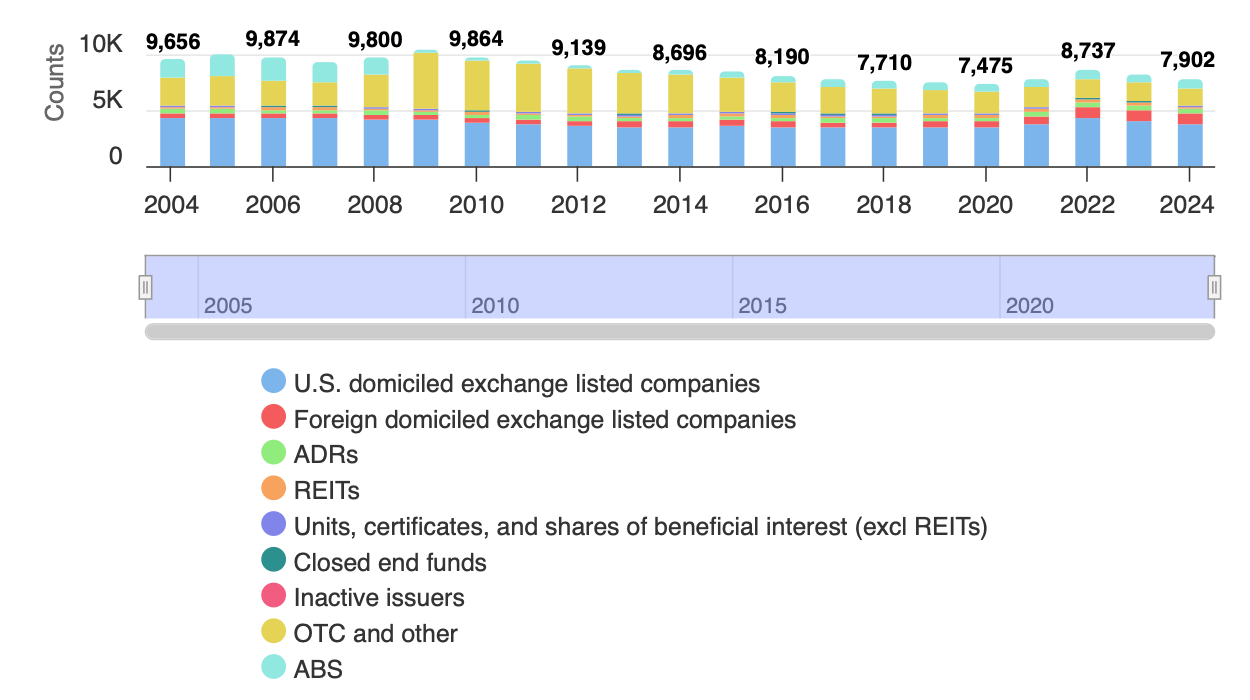

In the Washington Post, George Mason law professor Todd Zywicki takes note of the steady drop in the number of publicly traded companies in the United States.

Since the late 1990s, the number of publicly traded companies has fallen by more than half. Initial public offerings, once a reliable engine of economic dynamism that let ordinary Americans invest in tomorrow’s great companies, have plummeted.

A Short Digression from the Department of Self-Promotion

By the way, I took note of the same phenomenon last fall:

Why do we Care?

Zywicki does not devote a lot of attention to the “who cares” question, although that’s doubtless due to the space limitations of the op-ed format. But despite the brevity of his comments, they are quite telling:

… this decline in public offerings limits Americans’ access to investment opportunities and shifts capital formation toward private markets that are largely inaccessible to ordinary investors. …

Innovative and new companies — artificial intelligence companies, in particular — have become the latest cash cow for securities lawyers. In turn, economists have found that innovation and economic growth are being impeded by this rising threat of litigation.

I concur.

The dramatic decline in publicly traded U.S. corporations has had serious consequences for the American economy’s dynamism and efficiency. Public equity markets have historically served as the primary mechanism for allocating capital to its most productive uses, with competitive pricing of shares reflecting the dispersed information and judgment of millions of investors. When companies remain private or are absorbed through M&A rather than going public, this price discovery function is impaired. Capital gets channeled instead through private equity and venture capital, which are accessible only to institutional investors and the ultra-wealthy, meaning that investment decisions affecting large swaths of the economy are made by a far narrower set of actors with less informational diversity. The result is a less efficient deployment of the nation’s capital stock and a greater concentration of economic decision-making power.

The consequences for ordinary Americans are equally troubling. Historically, the public equity markets were a vehicle through which middle-class households could accumulate wealth by owning stakes in growing companies. As firms stay private longer — or never go public at all — the wealth generated during the high-growth phases of corporate development accrues almost exclusively to venture capitalists, private equity funds, and their wealthy limited partners. By the time a company does reach public markets (if it ever does), much of the appreciation has already occurred. This dynamic has contributed to widening wealth inequality, since participation in private markets is largely limited to accredited investors who already meet high income or net-worth thresholds. The shrinkage of the public markets thus represents not just an economic efficiency loss but a structural barrier that prevents ordinary Americans from sharing in the gains of entrepreneurial capitalism.

Zywicki’s Explanation

If Zywicki and I are right that the decline in the number of public corporations is bad for both the investing public and entrepreneurs, why is it happening?

Zywicki lays the blame at the feet of trial lawyers, especially securities class action plaintiff lawyers:

Meritless securities suits have become a reliable way for trial lawyers to extract massive settlements from public companies, often with little connection to actual investor harm. …

A company accused of making a false statement may already face a direct fraud lawsuit over the underlying conduct. Then, when that allegation becomes public and the stock price falls, a separate class of shareholders, often represented by the same plaintiffs’ firm, files suit. This effectively allows trial lawyers to recycle the same allegation into a second round of litigation. If settled, the company pays twice for the same alleged wrong, irrespective of whether either claim was ever proved on the merits.

Allowing this to continue unabated serves one constituency: trial lawyers, who pocket exorbitant fees while companies, workers and consumers absorb the real costs.

My Take

I largely agree with Zywicki. Indeed, over a decade ago I contributed a chapter to a wonderful—albeit somewhat depressing book The American Illness: Essays on the Rule of Law (Amazon Link):

This provocative book brings together twenty-plus contributors from the fields of law, economics, and international relations to look at whether the U.S. legal system is contributing to the country’s long postwar decline. The book provides a comprehensive overview of the interactions between economics and the law—in such areas as corruption, business regulation, and federalism—and explains how our system works differently from the one in most countries, with contradictory and hard to understand business regulations, tort laws that vary from state to state, and surprising judicial interpretations of clearly written contracts. This imposes far heavier litigation costs on American companies and hampers economic growth.

My chapter was How American Corporate and Securities Law Drives Business Offshore, in which I argued that:

During the first half of the last decade, evidence accumulated that the U.S. capital markets were becoming less competitive relative to their major competitors. The evidence reviewed herein confirms that it was not corporate governance as such that was the problem, but rather corporate governance regulation. In particular, attention focused on such issues as the massive growth in corporate and securities litigation risk and the increasing complexity and cost of the U.S. regulatory scheme.

Tentative efforts towards deregulation largely fell by the wayside in the wake of the financial crisis of 2007-2008. Instead, massive new regulations came into being, especially in the Dodd Frank Act. The competitive position of U.S. capital markets, however, continues to decline.

This essay argues that litigation and regulatory reform remain essential if U.S. capital markets are to retain their leadership position. Unfortunately, the article concludes that federal corporate governance regulation follows a ratchet effect, in which the regulatory scheme becomes more complex with each financial crisis. If so, significant reform may be difficult to achieve.

The Role of Litigation

With respect to the role litigation plays in the decline of public companies, I argued that:

An effective anti-fraud regime has obvious benefits. It serves to compensate defrauded investors. It deters fraud. It provides a bond making issuer disclosures more credible and thereby lowers the cost of capital. The question remains, however, whether the current U.S. anti-fraud regime imposes costs that may outweigh or, at least, reduce these benefits.

An affirmative answer to that question is suggested by a survey of global financial services executives, which found that the litigious nature of U.S. society and capital markets has a negative impact on the competitiveness of those markets. The key problem appears to be the prevalence of private party securities fraud class actions, which do not exist in most other major capital market jurisdictions.

Between 1997 and 2005 there was a steady increase in both the number of securities class action filings and the average settlement value of those suits. The total amount paid in securities class actions peaked in 2006 at over $10 billion, even excluding the massive $7 billion Enron settlement. The vast majority of such settlement payments historically have been made either by issuers or their insurers, rather than by individual defendants. As a result, the vast bulk of securities settlement payments come out of the corporate treasury, either directly or indirectly in the form of higher insurance premia. In either case, settlement payments reduce the value of the residual claim on the corporation’s assets and earnings. In effect, the company’s current shareholders pay the settlement, not the directors or officers who actually committed the alleged wrongdoing.

The effect of securities class actions thus is a wealth transfer from the company’s current shareholders to those who held the shares at the time of the alleged wrongdoing. In the case of a diversified investor, such transfers are likely to be a net wash, as the investor is unlikely to be systematically on one side of the transfer rather than the other. Because there are substantial transaction costs associated with such transfers, moreover, the diversified investor is likely to experience an overall loss of wealth as a result of the private securities class actions. Legal fees to plaintiff counsel typically take 25-35% of any monetary class action settlement, for example, and the corporation’s defense costs are likely comparable in magnitude.

The circularity inherent in the securities class action process reduces the effectiveness of private anti-fraud litigation as both a deterrent and means of compensation. As to deterrence, because it is the company and not the individual wrongdoers that pays in the vast majority of cases, the system fails to directly punish those individuals. As to compensation, the transaction costs associated with securities litigation ensure that investors are unlikely to recover the full amount of their claims. Indeed, there is evidence that investors recover only two to three percent of their economic losses through class actions.

The analysis to this point has implicitly assumed that all securities fraud class actions are meritorious. When one considers the potential for frivolous or nuisance litigation, the potential impact of litigation on the capital markets is compounded. …

The litigation risk problem is not limited to securities class actions. We see essentially identical concerns in areas such as state corporate law derivative litigation. …

Like securities class actions, derivative litigation mainly serves as a means of transferring wealth from investors to lawyers. At best, derivative suits take money out of the corporate treasury and return it to shareholders minus substantial legal fees. In many cases, moreover, little if any money is returned to the shareholders, but legal fees are almost always paid.

Other Factors

Although I’m confident litigation has been a major factor in the decline of US public markets, I don’t think it is the only factor.

Over-Regulation

The regulatory burden from federal law has had a cumulative effect that significantly contributed to the decline in public companies, though the impact varies by company size and regulatory framework. Sarbanes-Oxley appears to be the most significant regulatory contributor to public company decline, with documented evidence of companies specifically citing SOX as a reason for delisting. Dodd-Frank had a more sector-specific impact, primarily affecting financial institutions through massive increases in regulatory requirements. More generally, cumulative SEC regulations create a “death by a thousand cuts” effect, particularly for smaller companies.

Having said that, however, I must confess that the evidence suggests that over-regulation is not the main driver of the decline in public companies. But while over-regulation likely is not the primary numerical cause of the decline, these regulations have fundamentally altered the cost-benefit calculus of being public, particularly for smaller companies, making private markets relatively more attractive and contributing to companies staying private longer.

Still Others

As I discussed in my Substack last fall, other factors include the rise of private equity and venture capital, the shift towards intangible assets, and industry consolidation.

Conclusion

There is no doubt that the number of US public corporations has shrunk. As with most economic trends, the reasons driving this long-standing trend are multiple and complex. As Zywicki so cogently argued, however, the litigation risks that public corporations face is undoubtedly a major component.

It’s long since time that courts and lawmakers step up and address the problem.